The Legal Risk Hidden in Every Used Boat’s Past

Before You Buy That Boat, Know What Liability You’re Inheriting

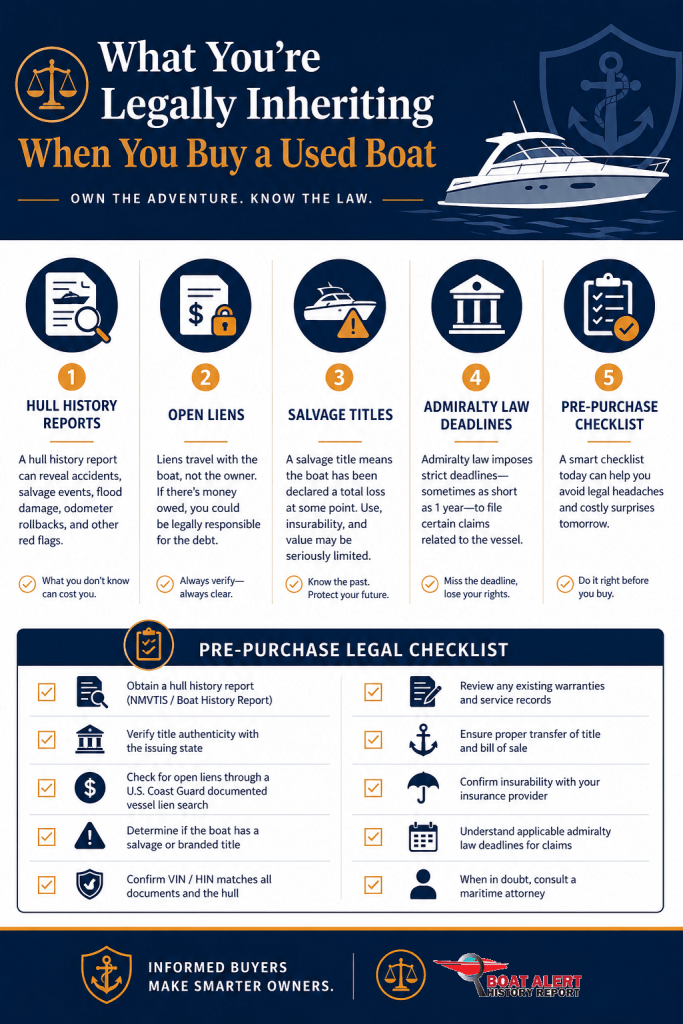

Most people buying a used boat worry about whether the engine runs and whether the price is fair. Few think about what they’re legally inheriting the moment they sign the title. A clean hull and a fresh coat of wax can hide structural damage, unresolved liens, and a history of repairs that never made it into any disclosure — and once that boat is in your name, its past becomes your problem.

A boat history report is one of the cheapest ways to find out what you’re actually buying before it’s too late to walk away.

What a history report actually tells you

Pulling a report by Hull Identification Number (HIN) is the marine equivalent of a vehicle history check. A service like Boat Alert runs that HIN across roughly 90 databases and can surface:

- Salvage or rebuilt titles: a boat declared a total loss by an insurer and later patching back together

- Accident and damage history: collisions, groundings, fires, and storm damage that may have been repaired cosmetically but not structurally

- Open liens and loan records: money still owed against the boat that can follow it to a new owner

- Registration and ownership trail: frequent state-to-state moves or title gaps that hint at a problem being shuffled out of sight

- Theft and recovery records: a recovered stolen vessel can carry a clouded title for years

Any one of these can turn a “great deal” into a boat you can’t insure, can’t resell — and one that could expose you to serious legal liability.

When you buy the boat, you buy the history

Here’s what most buyers never consider until something goes wrong: a vessel’s past doesn’t stay in the past.

If you purchase a boat with undisclosed structural damage and a passenger is later hurt because of a failure traceable to that prior damage, questions about who knew what — and when — can become legally significant very quickly. The liability picture gets even more complicated if you’re the one injured: a hidden defect from a previous repair, negligence by a prior owner, or corners cut during a rebuild can all factor into what happened and who bears responsibility.

What makes this especially consequential is that recreational boating injuries don’t follow the same legal rules as a car accident. They fall under admiralty and maritime law — a specialized area with its own deadlines, procedures, and standards that routinely catch injured parties off guard. Missing those windows, or allowing key evidence to disappear, can fundamentally change the outcome of a claim.

If you or someone aboard is ever seriously hurt on the water, speaking early with attorneys who handle these cases specifically matters. Firms like BoatLaw LLP focus exclusively on maritime injury claims and can help you understand your options while evidence — the boat itself, its repair history, and records of prior damage — is still available and intact.

The lien you didn’t know about can cost you the boat

An open lien is one of the most financially punishing surprises in a used boat purchase — and one of the most preventable.

When a previous owner borrowed against a vessel and didn’t pay off the loan, that debt can survive the sale. Marine lenders and some commercial creditors hold liens that attach to the boat itself, not just the person who borrowed. Buy a boat with an undisclosed lien and you may find yourself facing a creditor who has a legal claim to a vessel you paid for in good faith.

Unlike real estate, where title insurance is standard and lien searches are built into the closing process, private boat sales often skip these protections entirely. There’s no escrow officer double-checking the paperwork. The buyer and seller shake hands, money changes hands, and the problem surfaces later — sometimes when you try to register the boat in your name, sometimes when a lender’s collections process reaches out to the new registered owner.

A history report flags recorded liens, but the step that actually protects you is verifying the lien is satisfied — in writing, with documentation — before the transaction closes. If a seller can’t produce a lien release or payoff confirmation, that’s not a minor administrative gap. It’s a reason to walk away or place funds in escrow until the debt is cleared.

Salvage titles and the insurance trap

A boat with a salvage title — one that was declared a total loss by an insurer — creates a problem that outlasts the original damage: getting it properly insured after you buy it.

Many standard marine insurers will decline to cover a vessel with a salvage history, or will cover it only under heavily restricted terms. Some will write a policy at purchase and then deny a claim later when the salvage record surfaces during the claims investigation. That gap between having a policy and having actual coverage is where buyers get hurt. Accidents are on the rise too.

The risk compounds if the boat is later involved in an incident and causes damage to another vessel, a marina, or injures a third party. A boat that can’t pay out a liability claim because its coverage was voided leaves the owner personally exposed. In a maritime context, personal exposure can be substantial — damage to other vessels, environmental cleanup costs, and injury claims can add up far beyond what most recreational boaters anticipate.

Before buying any vessel with a salvage or rebuilt title, get written confirmation from a marine insurer that they will cover the specific vessel, at the coverage levels you need, before you close the sale. Don’t assume the policy you’re quoted is the coverage you’ll actually receive when it matters.

Prior commercial use: a liability history you can’t see on the surface

A boat that spent years as a charter vessel, a rental, or a dive boat before entering the private resale market carries a usage history that affects far more than just wear and tear.

Commercial marine operators are subject to different inspection, maintenance, and safety equipment standards than recreational owners. A vessel that cycled through heavy passenger loads, was maintained to the minimum standard required for a certificate of inspection, or was involved in incidents that were handled quietly through a commercial operator’s insurer may show little of that history on its hull. But the cumulative stress of that use — on the engines, the through-hulls, the electrical systems, the structural members — doesn’t disappear when the boat is sold private.

There’s also a documentation issue. Commercial vessels sometimes transition from USCG documentation to state registration when they move into the private market, which can reset parts of the visible paper trail. A thorough HIN search combined with a check of USCG documentation records can help surface this kind of history. So can asking direct questions: where was this boat homeported, was it ever operated commercially, and does the seller have maintenance logs going back more than a season or two?

A qualified marine surveyor with experience in former charter or commercial vessels is especially valuable here. They know the systems that get pushed hardest in commercial service and the repairs that tend to get deferred when a boat is generating revenue.

Why salvage and damage history is a safety issue, not just a paperwork one

It’s tempting to treat a damage flag on a history report as a negotiating chip and move on. That’s a mistake.

A boat that has been through a serious collision or grounding may have compromised stringers, a stressed transom, or hidden hull delamination. Those failures don’t show up at the dock. They show up offshore, under power, in a following sea — when you have the least margin for error and the most to lose. And if something does fail, the history of that prior damage becomes directly relevant to any legal claim that follows.

A salvage or heavy-damage record is a signal to slow down and bring in a qualified marine surveyor before going any further. Pairing the history report with a physical inspection from an independent surveyor is how careful buyers protect both their investment and the people who will be on the water with them.

What “as-is” really means — and what it doesn’t

Many private boat sales include an “as-is” clause, and sellers often treat this as a blanket shield against any future complaint. It isn’t.

“As-is” in a boat sale means the buyer accepts the vessel in its current condition and generally waives claims based on defects that could have been discovered through reasonable inspection. It does not protect a seller who actively concealed a known defect. It does not protect against fraud. And it does not transfer liability for injuries caused by a pre-existing structural failure that the seller knew about and didn’t disclose.

For the buyer, “as-is” is also a signal, not a reassurance. A seller pushing hard for an as-is sale with no documentation, no survey opportunity, and no disclosure of history may be trying to move a problem rather than sell a boat. The more pressure there is to skip due diligence, the more reason there is to insist on it.

If a seller discloses a defect in writing and the buyer accepts it knowingly, that’s a legitimate as-is transaction. If a seller conceals known damage, a signed as-is clause won’t protect them — and getting that disclosure in writing creates the paper trail that makes the distinction clear if things go wrong later.

Ask the seller if they kept detailed records. Some People use TheBoatApp. It is an all-in-one boat management platform (web, iOS, and Android) that centralizes everything a boat owner needs in one place — online and offline. It covers eight core areas: a logbook for voyages and weather logs (with Google Maps/Windy integration), inventory tracking for equipment and safety gear with expiry alerts, task and checklist management for maintenance, automated alerts, cloud document storage, cost tracking, and crew/team sharing. The core idea: one organized, backed-up hub for all your boating data, accessible from any device.

A pre-purchase checklist that also protects you legally

Before you buy any used boat:

- Pull the full history report by HIN and read it completely, not just the summary

- Match the HIN on the report to the physical hull, the title, and the registration — mismatches are a serious red flag

- Hire an independent marine surveyor, especially if the report shows any damage, salvage, or rebuilt history

- Verify there are no open liens before any money changes hands and get lien releases in writing

- Confirm insurability before closing — especially for any vessel with a salvage or rebuilt title

- Ask directly about commercial use history and request maintenance logs going back as far as available

- Get every disclosure in writing, including the seller’s account of any known past damage

- Be skeptical of pressure to skip steps — urgency and “as-is” pressure are due diligence red flags, not normal sales tactics

That written disclosure matters more than most buyers realize. If a seller conceals a known defect and something goes wrong later, that paper trail — or the absence of one — can be central to establishing what happened and who is responsible.

Frequently Asked Legal Boat Questions

Who Can Be Held Liable After a Boating Accident

Liability in a maritime injury case can fall on more than one party. Depending on the facts, responsible parties may include:

- The vessel’s owner — particularly where inadequate maintenance, safety failures, or a history of unrepaired structural damage contributed to the accident

- The captain or crew — if their negligence or errors directly caused the incident

- The operating company — if they failed to meet safety standards, properly inspect the vessel, or adequately train personnel

- A prior owner or seller — if they knowingly concealed structural damage or misrepresented the vessel’s history and that damage later caused a failure

- A repair company — if a previous fix was performed negligently and that substandard repair contributed to the accident

- Third-party operators — in a collision or multi-vessel incident, other boat operators may share or bear full liability

Q: How do I find the Hull Identification Number (HIN) on a boat? The HIN is a 12-character alphanumeric code required on all boats manufactured after November 1, 1972. It’s permanently affixed to the upper starboard (right) side of the transom — the flat rear surface of the hull. A duplicate HIN is also hidden somewhere on the interior of the boat, typically under a fitting or inside a locker. If the transom HIN has been removed, altered, or is difficult to read, treat that as a serious red flag and do not proceed without investigating further.

Q: Can I run a boat history report on any vessel? Most history report services work on motorized recreational vessels registered in the United States. Coverage is strongest for boats manufactured after 1972, since the HIN system wasn’t standardized before then. Older vessels, documented commercial ships, and some foreign-flagged boats may return limited results. If you’re buying a documented vessel, you can also search USCG documentation records directly through the National Vessel Documentation Center for ownership and lien history.

Q: What’s the difference between a salvage title and a rebuilt title? A salvage title is issued when an insurer declares a vessel a total loss — meaning the cost to repair it exceeded a threshold percentage of its value. A rebuilt title is issued after that same vessel has been repaired and passed a state inspection to return to legal operation. Both are red flags, but for different reasons. A salvage title means the boat hasn’t been certified as repaired. A rebuilt title means it has — but the quality of those repairs is only as good as whoever did the work, and a marine surveyor is the only way to assess that independently.

Q: Do open liens automatically transfer to a new owner when a boat is sold? In most cases, yes. Marine liens attach to the vessel itself, not to the person who incurred the debt. That means a lender or creditor with a recorded lien may have a legal claim against the boat regardless of who currently owns it. This is why verifying and clearing all liens before closing is essential — not optional. If a seller cannot produce a lien release or payoff letter, hold funds in escrow until the debt is documented as satisfied.

Q: Is a marine survey the same as a boat history report? No, and you need both. A history report is a records-based search — it tells you what’s been officially reported, documented, or recorded about a vessel’s past. A marine survey is a physical inspection conducted by a qualified professional who boards the boat, inspects the hull, systems, and structure, and gives you an independent condition assessment. The report tells you what happened. The survey tells you what it looks like now. Neither one alone gives you the complete picture.

Q: What is admiralty and maritime law, and why does it apply to my recreational boat? Admiralty and maritime law is the body of federal law that governs activities on navigable waters — including recreational boating accidents. It applies regardless of whether you’re on a commercial ship or a personal fishing boat. This area of law has its own statutes of limitations, procedural rules, and standards of liability that differ significantly from state personal injury law. Deadlines can be shorter, rules around preserving evidence are stricter, and the legal theories involved are distinct. If you’re ever injured in a boating accident, assuming your regular personal injury attorney has the right expertise can be a costly mistake. Maritime claims carry strict filing windows that differ significantly from standard personal injury law. Jones Act negligence and unseaworthiness claims must generally be filed within three years. Claims under the Longshore and Harbor Workers’ Compensation Act carry a one-year deadline. Missing these cutoffs can eliminate your right to compensation entirely — which is why contacting a maritime attorney early, before evidence disappears and deadlines pass, is so important.

Q: Can a seller’s “as-is” clause protect them if I’m injured due to hidden damage? Generally, no. An as-is clause protects a seller from claims based on defects the buyer could have discovered through reasonable inspection. It does not shield a seller who knowingly concealed a structural defect, misrepresented the boat’s history, or committed fraud. If you’re injured because of damage the seller knew about and didn’t disclose, that as-is clause is unlikely to be a complete defense. Getting every known defect disclosed in writing before closing is important for both parties — it defines exactly what was known and accepted, and what wasn’t.

Q: What should I do if I’m injured in a boating accident involving a vessel with hidden damage history? Act quickly and preserve everything. Do not allow the boat to be repaired, moved, or disposed of before it can be inspected by an expert. Document the scene, the damage, and any visible condition of the vessel. Gather any records you have — the history report, the survey, the bill of sale, and any written disclosures. Then contact an attorney who specializes in maritime injury law as soon as possible. Firms like BoatLaw LLP handle exactly these kinds of cases and can advise you on evidence preservation, applicable deadlines, and your legal options before critical information disappears.

Q: How much does a boat history report cost, and is it worth it? A single report typically runs between $15 and $40 depending on the service and level of detail. That’s a negligible cost relative to even a modest used boat purchase — and a fraction of what a single undisclosed lien, a denied insurance claim, or a structural failure could cost you financially or legally. Think of it the same way you’d think of a home inspection: skipping it doesn’t save money, it just moves the risk from the seller to you.

Q: What if the boat I’m buying has no reported history at all — is that a good sign? Not necessarily. A clean report means no negative events were officially reported or recorded — it doesn’t mean nothing happened. Unreported accidents, repairs done outside of insurance claims, and informal ownership transfers can all leave gaps in the record. A clean history report is a good starting point, not a finish line. It should always be paired with a physical survey and thorough questioning of the seller about the vessel’s use, storage, and maintenance history.

op Hidden Boat Liabilities

- Wreck Removal & Environmental Cleanup: If your boat sinks, you are legally responsible for removing the wreckage and paying for any fuel or oil spills. Standard boat policies often cap this, but coverage is available through Chubb Marine Liability Insurance or specialized programs.

- Family & Passenger Injury: Many boaters assume their guests are covered, but family members are often excluded from liability payouts under standard recreational policies.

- Homeowners Policy Traps: People in the Laval/Montreal area often assume their home insurance covers their watercraft. However, home insurance usually limits coverage to very small, low-horsepower boats. A dedicated ClicAssure.com Quote Comparison will help you check if you need standalone watercraft liability coverage.

- Permitted Operators vs. Permitted Passengers: Allowing an unlicensed or underage friend to drive your boat—or having more passengers onboard than the U.S. Coast Guard/Transport Canada capacity plate permits—can void your liability coverage entirely.

- Watersport Exclusions: Towing tubers, wakeboarders, or skiers increases liability risk. You must verify that your policy explicitly covers these activities.

- Navigational Limits: If you take your boat on waters outside your insurer’s approved geographical limits (e.g., crossing into international waters or navigating unapproved Great Lakes), or if your boat is left in the water past the winterizing date, a resulting claim can be denied.

- Admiralty and maritime law overview

https://www.law.cornell.edu/wex/admiralty - Jones Act statute (46 U.S.C. § 30104)

https://www.law.cornell.edu/uscode/text/46/30104 - Death on the High Seas Act (DOHSA)

https://www.law.cornell.edu/uscode/text/46/30301 - Limitation of Liability Act

https://www.law.cornell.edu/uscode/text/46/30501

#BoatSafety #BoatLien #liability #BoatLaw #maritimeInjury

Read Related Articles:

- How to Sell a Boat in Pennsylvania

- Beware: Boat Consignment Fraud [With Examples]

- Best Marine Surveyors in Denver

- All you wanted to know about Hull ID Numbers

- Best Boat Dealers in Ohio

Categories: To learn more about Boat-Alert.com History Reports for used boats and free boat hull number check visit: www.Boat-Alert.com