Is Your Boat Insurance adequate? – Checkup time!

Why Most Boat Insurance Policies Fall Short

A standard homeowner’s insurance policy typically covers small, low-value watercraft, but once you own a vessel with a motor or one valued above a few thousand dollars, you need a dedicated marine policy. Even many standalone boat policies contain subtle gaps that only surface when something goes wrong on the water.

According to the Boat Owners Association of The United States (BoatUS), the three most dangerous coverage gaps in recreational boat policies involve consequential damage, salvage costs, and hurricane preparation. Beyond those, liability limits, medical payments, and uninsured boater coverage are frequently underestimated as well.

Before the boating season begins, take 30 minutes to read your declarations page against the checklist below. It could save you tens of thousands of dollars.

The 6 Critical Boat Insurance Coverages to Check

⚓1. Consequential Damage Coverage (High Risk Gap)

Large incidents — especially sinkings — are frequently caused by the failure of small, inexpensive parts below the waterline. Cracked rubber outdrive bellows, corroded thru-hulls, and failed shaft seals are common culprits. The defective part itself is typically excluded from coverage (it wore out), but consequential damage coverage pays for the resulting loss — repairs, emergency pumping, or even a total loss settlement — up to your policy’s selected limits.

Without this coverage, your insurer could deny the sinking claim by arguing the loss stemmed from a maintenance-related defect. This is one of the most common reasons boat insurance claims are denied.

What to ask your insurer: “Does my policy include consequential damage coverage, and what causes of loss trigger it?” Look for language covering sinking, fire, explosion, demasting, collision, and stranding.

🚢2. Salvage Coverage (High Risk Gap)

When a boat runs aground, capsizes, or sinks in a navigable waterway, the owner is legally obligated to arrange its removal. Salvage operations can easily cost $10,000–$50,000 or more depending on the size of the vessel and location.

Some policies subtract salvage costs directly from your hull-value coverage. If your boat is insured for $60,000 and salvage runs $15,000, you’re left with only $45,000 to repair or replace a boat that may be a total loss. Other policies offer a small “salvage sublimit” — for example, 10% of hull value — that rarely covers the actual bill.

What to look for: Salvage coverage that is separate from and equal to your hull-value limit. This means salvage costs do not reduce your repair or replacement payout.

🌀3. Hurricane Haulout Coverage (Regional Risk)

For boat owners in the Gulf of Mexico, Atlantic Coast, and Caribbean, hauling a vessel before a hurricane is the single most effective way to prevent catastrophic loss. However, professional haulout, blocking, shrink-wrapping, and hurricane preparation can cost $500–$2,000 or more, depending on the vessel.

Hurricane haulout coverage reimburses a portion of those costs even if the storm never makes landfall or causes any damage to your boat. The BoatUS Marine Insurance Program, for example, pays 50% of labor costs up to $1,000 for hauling or moving the boat to a safe location — without penalizing the policyholder’s premium at renewal.

Who needs it: Any boat owner whose vessel is kept in Florida, the Gulf Coast, the Carolinas, or any Caribbean island during hurricane season (June–November).

⚖️4. Liability Coverage — Are Your Limits High Enough? (High Risk Gap)

Bodily injury and property damage liability is the coverage that pays if you injure another person or damage their property while operating your boat. Many older policies carry only $100,000 in liability limits — a figure that could be exhausted by a single serious accident involving medical bills, lost wages, and pain and suffering claims.

Recommended minimums: $300,000 for most recreational powerboats; $500,000 or more for high-speed vessels, large sailboats, or anyone who charters their boat. A marine umbrella policy can extend your coverage to $1 million or more at a relatively low annual cost.

🏥5. Medical Payments Coverage

Medical payments coverage (sometimes called “guest passenger liability”) pays for reasonable medical expenses incurred by passengers on your boat regardless of fault. Without it, an injured guest would need to prove you were negligent before your liability coverage activates — and that can take years in litigation.

Coverage typically ranges from $1,000 to $10,000 per person. Given the cost of emergency services and a single night in a hospital, the highest available limit is usually worth the modest additional premium.

🚤6. Uninsured/Underinsured Boater Coverage

Unlike auto insurance, many states do not require boat owners to carry liability insurance at all. This means a significant percentage of boats on the water are completely uninsured. If an uninsured boater collides with you and injures you or your passengers, your only financial recourse may be suing a defendant with no ability to pay.

Uninsured boater coverage protects you in exactly this scenario, covering medical expenses and sometimes property damage when the at-fault party has no insurance or insufficient coverage.

Ready to review your coverage?

Get a fast, competitive boat insurance quote from Roamly — a modern insurer built specifically for outdoor enthusiasts and liveaboard cruisers.

Get your boat insurance quote from Roamly today.

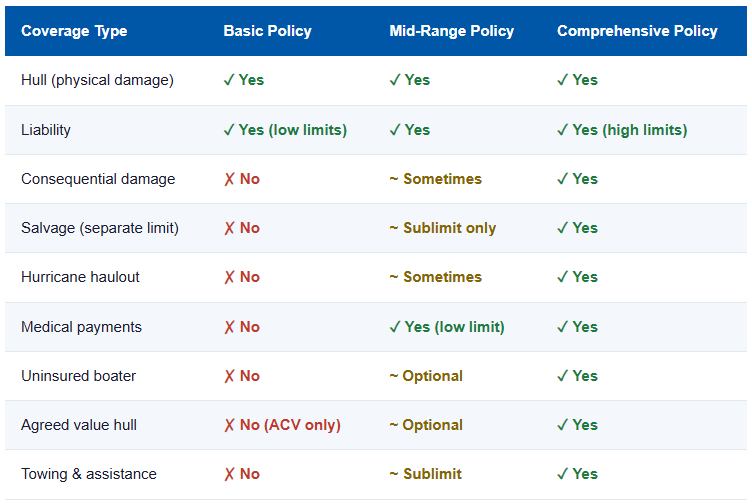

Boat Insurance Coverage Comparison: What Policies Typically Include

| Coverage Type | Basic Policy | Mid-Range Policy | Comprehensive Policy |

|---|---|---|---|

| Hull (physical damage) | ✓ Yes | ✓ Yes | ✓ Yes |

| Liability | ✓ Yes (low limits) | ✓ Yes | ✓ Yes (high limits) |

| Consequential damage | ✗ No | ~ Sometimes | ✓ Yes |

| Salvage (separate limit) | ✗ No | ~ Sublimit only | ✓ Yes |

| Hurricane haulout | ✗ No | ~ Sometimes | ✓ Yes |

| Medical payments | ✗ No | ✓ Yes (low limit) | ✓ Yes |

| Uninsured boater | ✗ No | ~ Optional | ✓ Yes |

| Agreed value hull | ✗ No (ACV only) | ~ Optional | ✓ Yes |

| Towing & assistance | ✗ No | ~ Sublimit | ✓ Yes |

⚠️ Agreed Value vs. Actual Cash Value: Many basic policies pay out “actual cash value” (ACV) after depreciation, not the replacement cost of your boat. On a 10-year-old vessel, ACV may be 40–60% less than what you need to replace it. Look for an agreed value policy, where you and the insurer agree on the boat’s value at the time of purchase — and that is what you receive if it’s a total loss.

Printable Boat Insurance Checklist

Use this checklist when reviewing your policy documents or speaking with your insurance agent:

📋 Annual Boat Insurance Review Checklist

- Locate your current declarations page and note all coverage limits and deductibles

- Confirm hull coverage is on an agreed value basis (not actual cash value)

- Verify consequential damage coverage is included and note what triggers it

- Check that salvage coverage is a separate limit equal to your hull value

- Confirm hurricane haulout coverage if you are in a hurricane-prone region

- Review your liability limits — are they at least $300,000?

- Check for medical payments coverage and note the per-person limit

- Confirm uninsured boater coverage is included

- Review the geographic coverage area — does it cover all waters where you operate?

- Check your liveaboard or charter exclusions if applicable

- Confirm your policy covers trailer transport if you trailer your boat

- Review personal property coverage for electronics, fishing gear, and safety equipment

- Note your policy’s lay-up period — does it match your actual storage dates?

- Run a HIN history report if you recently purchased a used boat to confirm there are no liens or reported incidents that affect insurability

When Should You Update Your Boat Insurance Policy?

Many boat owners set their policy and forget it for years. That approach creates real risk. Review your coverage whenever any of the following occur:

Major engine or equipment upgrades. If you’ve added a new outboard, a T-top, a bow thruster, or upgraded electronics, your hull value has likely increased. Notify your insurer to avoid being underinsured.

Change in use or cruising range. Planning an offshore passage or a trip to the Bahamas? Most coastal policies have geographic limits. Extended cruising often requires a rider or endorsement, and some insurers require advance notice of blue-water passages.

You start chartering the boat. Personal boat insurance policies typically exclude commercial use. If you’re renting the boat through a platform or peer-to-peer charter service, you need a policy that explicitly covers commercial charters.

You move to a different state. State regulations and minimum coverage requirements differ. Some states with aggressive litigation environments warrant higher liability limits.

Your boat’s market value changes significantly. Boat values have fluctuated considerably since 2020. If your boat has appreciated — or depreciated — make sure your insured value is updated to match.

How Boat History Affects Your Insurance

If you recently purchased a used boat, the vessel’s history can affect both your insurability and your premium. Boats with prior accident reports, salvage titles, outstanding liens, or unresolved theft records can be difficult or expensive to insure — and some insurers will deny claims if they discover an undisclosed incident after the fact.

Before finalizing a used boat purchase — or before renewing insurance on a vessel you acquired recently — run a HIN (Hull Identification Number) history report through Boat-Alert.com. The report checks multiple federal, state, and Canadian databases for accident records, ownership history, stolen vessel reports, and lien information.

Frequently Asked Questions About Boat Insurance Adequacy

What is consequential damage coverage for boats?

Consequential damage coverage pays for losses caused by the failure of a small, uncovered component — such as a cracked bellows or broken thru-hull — that leads to a major incident like sinking. The underlying part may not be covered, but the resulting damage (repairs or total loss) is.

Does standard boat insurance include salvage coverage?

Not always. Some policies deduct salvage costs from the insured hull value, leaving you with less money for repairs. Look for a policy where salvage coverage is separate from and equal to your hull-value limit.

What is hurricane haulout coverage?

Hurricane haulout coverage reimburses a portion of the labor costs to haul, prepare, and secure your boat before a storm. BoatUS, for example, pays 50% of labor costs up to $1,000 without penalizing your premium.

How much liability coverage do I need for my boat?

Most experts recommend a minimum of $300,000 in boat liability coverage. If you own a larger or faster vessel, or frequently boat in busy waterways, $500,000 or more — or a marine umbrella policy — is advisable.

When should I review my boat insurance policy?

Review your boat insurance at least once a year, ideally before the start of boating season. Also review after any major modification, engine upgrade, change in how you use the boat, or if you move to a new state or cruising region.

Is boat insurance required by law?

Most U.S. states do not legally require boat insurance for privately-owned recreational vessels (though a few states and some marina slip leases do require it). However, if your boat is financed, your lender will require insurance as a condition of the loan.

Final Thoughts

An adequate boat insurance policy isn’t just about having a policy — it’s about having the right coverage for how you actually use your boat. The six gaps described above — consequential damage, salvage, hurricane haulout, liability limits, medical payments, and uninsured boater coverage — are the most common sources of underinsurance claims among recreational boaters.

Use the checklist above to have a structured conversation with your insurance agent before your next boating season. And if you’re buying a used boat, pair your insurance review with a Boat-Alert HIN history report to make sure you’re insuring a boat with a clean history.

#Adequate #boat #insurance #UnderInsured

Categories: To learn more about Boat-Alert.com History Reports for used boats and boat hull lookup visit: www.Boat-Alert.com